Global Development

Making It Easier for Cash Transfer Recipients to Save

The Problem

Tanzania’s Productive Social Safety Net (PSSN) program provided bimonthly cash transfers to households in extreme poverty. In 2020, a new phase of the program focused on reducing long-term poverty by increasing opportunities to earn income and save for the future. While many cash transfer recipients wanted to invest in income-generating activities, their immediate needs made saving difficult to save enough to do so. The program needed to figure out how to help recipients translate their aspirations into concrete savings and productive investments.

Our Solution

Through in-depth focus groups, we identified five factors getting in recipients' way and designed low-cost, behaviorally-informed solutions to address each one:

Barrier

They didn't see themselves as people who could save

Solution

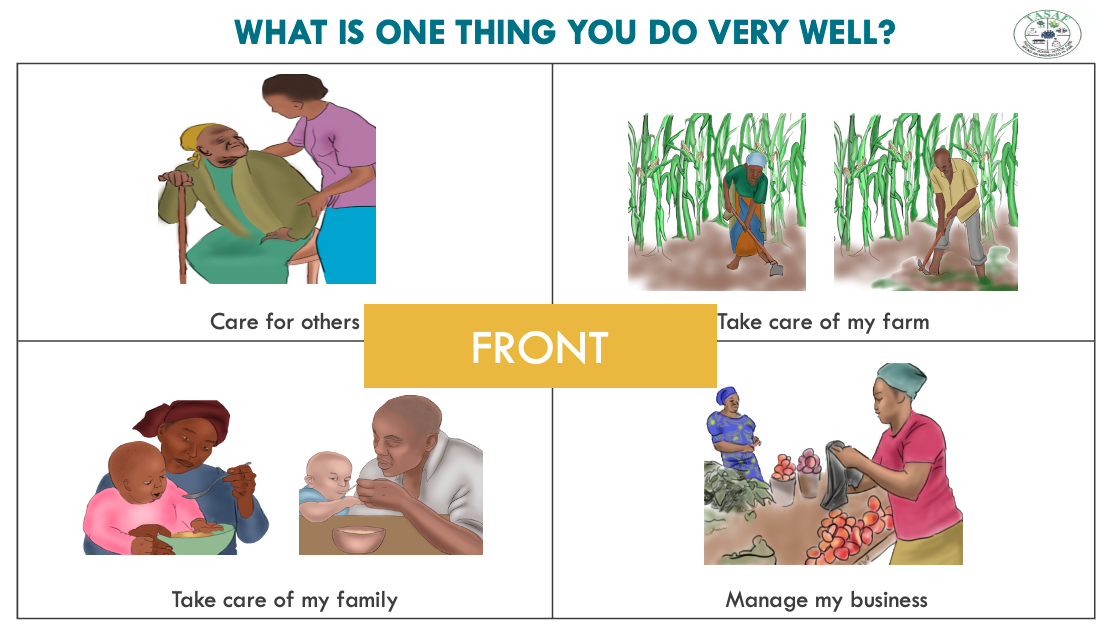

Self-affirmations: Created image cards to help recipients reflect on their values and skills to cultivate a positive mindset and reinforce that they can make a difference in their families' lives.

Barrier

They thought no one else was saving

Solution

Visible community norms: Posters showing examples of how other community members save and invest were put up at payment and gathering sites to normalize the behavior.

Barrier

They spent on whatever felt most urgent

Solution

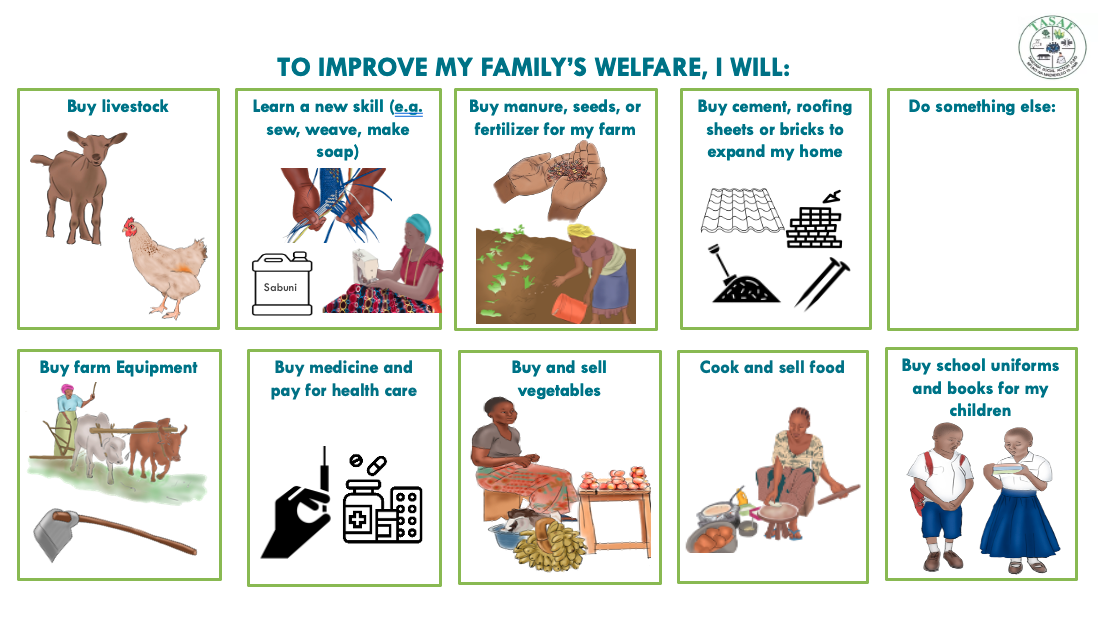

Set goals: Recipients created personal, concrete savings goals to make investment decisions easier after receiving their money.

Barrier

Financial stress made it hard to think ahead

Solution

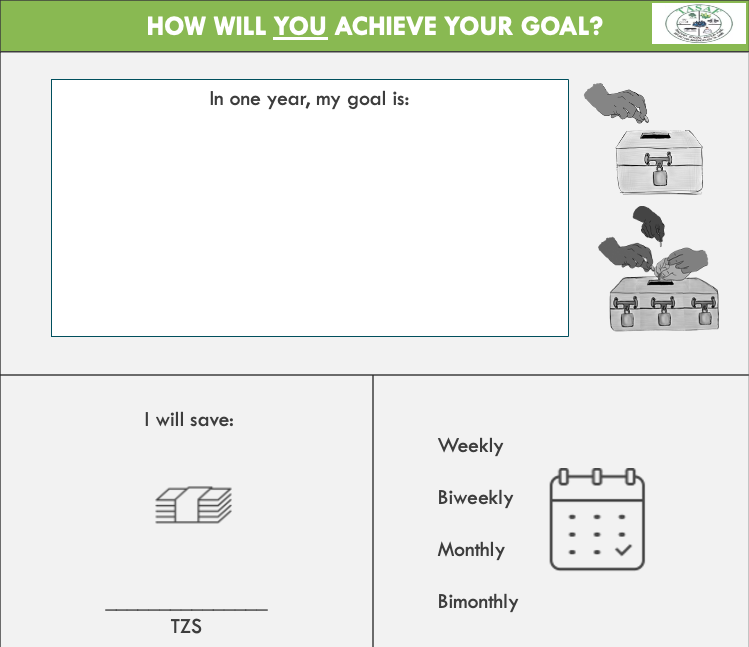

Made plans: Recipients identified simple, time-bound steps toward their goals, including how much to save from each transfer and had a tracker to celebrate progress and keep goals top-of-mind.

Barrier

Immediate needs and nearby vendors were too tempting

Solution

Separated funds: Pouches with two labeled pockets–consumption and savings–acted as a physical reminder to separate funds immediately after receiving payment.

The Results

These solutions were tested across 64 villages with over 2,600 recipients, with half the villages receiving the standard PSSN program and the other half receiving the standard program plus the tools we developed. Six months later, surveys assessed impact on goal-setting, planning, and follow-through–and the tools proved to be highly effective.

Recipients who received them, regardless of education level, were:

-

↑ 65%

more likely to have saved money

-

↑ 30%

more likely to have participated in savings groups

-

↑ 22%

more likely to have made productive investments in the past month

The tools were also highly cost-effective, proving to be about 1.5 times more effective at increasing savings than simply distributing equivalent cash amounts.

Based on these results, TASAF committed to scaling the tools throughout their program, with plans to reach 500,000-600,000 households across Tanzania.