Publications Toolkit/Guide, Financial Health Cameron French 7/1/25 Toolkit/Guide, Financial Health Cameron French 7/1/25 Checklist: Increasing Applications for Small Dollar Loans Read More Report, Financial Health Leslie Heilbrunn 6/1/25 Report, Financial Health Leslie Heilbrunn 6/1/25 Welcome Home Read More Financial Health, Report Cameron French 3/1/25 Financial Health, Report Cameron French 3/1/25 Small Business Owner Perspectives on Succession Planning: Survey Findings Read More Policy Brief & Fact Sheet, Financial Health Cameron French 3/1/25 Policy Brief & Fact Sheet, Financial Health Cameron French 3/1/25 Small Business Succession Planning Read More Webinar, Financial Health Cameron French 3/1/25 Webinar, Financial Health Cameron French 3/1/25 Small Business Owner Perspectives on Succession Planning Read More Financial Health, Report Leslie Heilbrunn 9/1/24 Financial Health, Report Leslie Heilbrunn 9/1/24 A Prime Opportunity Read More Report, Financial Health Cameron French 3/1/24 Report, Financial Health Cameron French 3/1/24 The Promise of Small-Dollar Loans for Banks and Consumers Read More Webinar, Financial Health Cameron French 7/13/23 Webinar, Financial Health Cameron French 7/13/23 Breaking Down Barriers to Affordable Credit Read More Toolkit/Guide, Financial Health Cameron French 7/1/23 Toolkit/Guide, Financial Health Cameron French 7/1/23 Increasing Applications for Small Dollar Loans Read More Research, Financial Health Leslie Heilbrunn 4/1/23 Research, Financial Health Leslie Heilbrunn 4/1/23 Saving for Retirement: A Real-World Test of Whether Seeing Photos of One’s Future Self Encourages Contributions Read More Research, Financial Health Leslie Heilbrunn 3/1/23 Research, Financial Health Leslie Heilbrunn 3/1/23 Identifying heterogeniety using recursive partitioning: evidence from SMS nudges encouraging voluntary retirement savings in Mexico Read More Project Brief, Financial Health Leslie Heilbrunn 2/1/20 Project Brief, Financial Health Leslie Heilbrunn 2/1/20 A Parent Engagement Guide to Improve Program Outreach Read More Project Brief, Financial Health Leslie Heilbrunn 10/1/19 Project Brief, Financial Health Leslie Heilbrunn 10/1/19 A “Save for College” Program Journey Read More Project Brief, Financial Health Cameron French 3/1/19 Project Brief, Financial Health Cameron French 3/1/19 The Financial Health Check: Helping People Build a Stronger Future Read More Policy Brief & Fact Sheet, Financial Health Cameron French 3/1/19 Policy Brief & Fact Sheet, Financial Health Cameron French 3/1/19 ¿Cómo es la experiencia decolaborar con un laboratoriode diseño conductual? Read More Project Brief, Financial Health Leslie Heilbrunn 3/1/19 Project Brief, Financial Health Leslie Heilbrunn 3/1/19 What Is It Like to Partner with a Behavioral Design Lab? Read More Report, Financial Health Leslie Heilbrunn 11/1/18 Report, Financial Health Leslie Heilbrunn 11/1/18 El uso de las ciencias del comportamiento para aumentar los ahorros para el retiro en México Read More Report, Financial Health Kelsey Egger 11/1/18 Report, Financial Health Kelsey Egger 11/1/18 Using Behavioral Science to Increase Retirement Savings in Mexico Read More Project Brief, Financial Health Leslie Heilbrunn 7/1/18 Project Brief, Financial Health Leslie Heilbrunn 7/1/18 The Financial Heuristics Training Read More Report, Financial Health Leslie Heilbrunn 10/1/15 Report, Financial Health Leslie Heilbrunn 10/1/15 Using Behavioral Science to Increase Retirement Savings Read More Older Posts

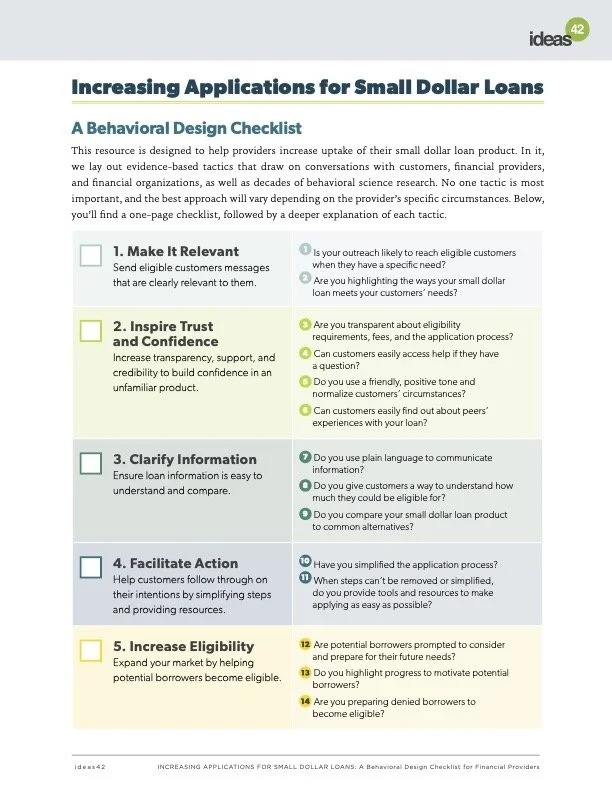

Toolkit/Guide, Financial Health Cameron French 7/1/25 Toolkit/Guide, Financial Health Cameron French 7/1/25 Checklist: Increasing Applications for Small Dollar Loans Read More

Report, Financial Health Leslie Heilbrunn 6/1/25 Report, Financial Health Leslie Heilbrunn 6/1/25 Welcome Home Read More

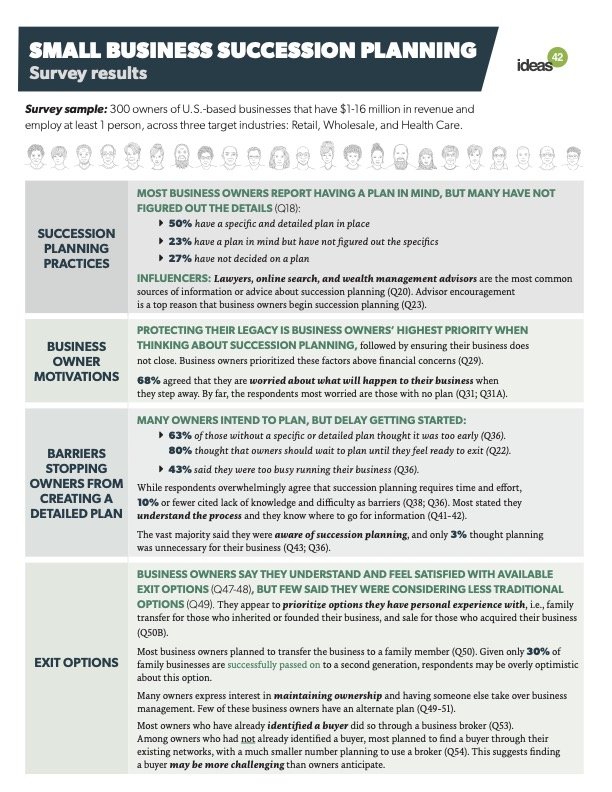

Financial Health, Report Cameron French 3/1/25 Financial Health, Report Cameron French 3/1/25 Small Business Owner Perspectives on Succession Planning: Survey Findings Read More

Policy Brief & Fact Sheet, Financial Health Cameron French 3/1/25 Policy Brief & Fact Sheet, Financial Health Cameron French 3/1/25 Small Business Succession Planning Read More

Webinar, Financial Health Cameron French 3/1/25 Webinar, Financial Health Cameron French 3/1/25 Small Business Owner Perspectives on Succession Planning Read More

Financial Health, Report Leslie Heilbrunn 9/1/24 Financial Health, Report Leslie Heilbrunn 9/1/24 A Prime Opportunity Read More

Report, Financial Health Cameron French 3/1/24 Report, Financial Health Cameron French 3/1/24 The Promise of Small-Dollar Loans for Banks and Consumers Read More

Webinar, Financial Health Cameron French 7/13/23 Webinar, Financial Health Cameron French 7/13/23 Breaking Down Barriers to Affordable Credit Read More

Toolkit/Guide, Financial Health Cameron French 7/1/23 Toolkit/Guide, Financial Health Cameron French 7/1/23 Increasing Applications for Small Dollar Loans Read More

Research, Financial Health Leslie Heilbrunn 4/1/23 Research, Financial Health Leslie Heilbrunn 4/1/23 Saving for Retirement: A Real-World Test of Whether Seeing Photos of One’s Future Self Encourages Contributions Read More

Research, Financial Health Leslie Heilbrunn 3/1/23 Research, Financial Health Leslie Heilbrunn 3/1/23 Identifying heterogeniety using recursive partitioning: evidence from SMS nudges encouraging voluntary retirement savings in Mexico Read More

Project Brief, Financial Health Leslie Heilbrunn 2/1/20 Project Brief, Financial Health Leslie Heilbrunn 2/1/20 A Parent Engagement Guide to Improve Program Outreach Read More

Project Brief, Financial Health Leslie Heilbrunn 10/1/19 Project Brief, Financial Health Leslie Heilbrunn 10/1/19 A “Save for College” Program Journey Read More

Project Brief, Financial Health Cameron French 3/1/19 Project Brief, Financial Health Cameron French 3/1/19 The Financial Health Check: Helping People Build a Stronger Future Read More

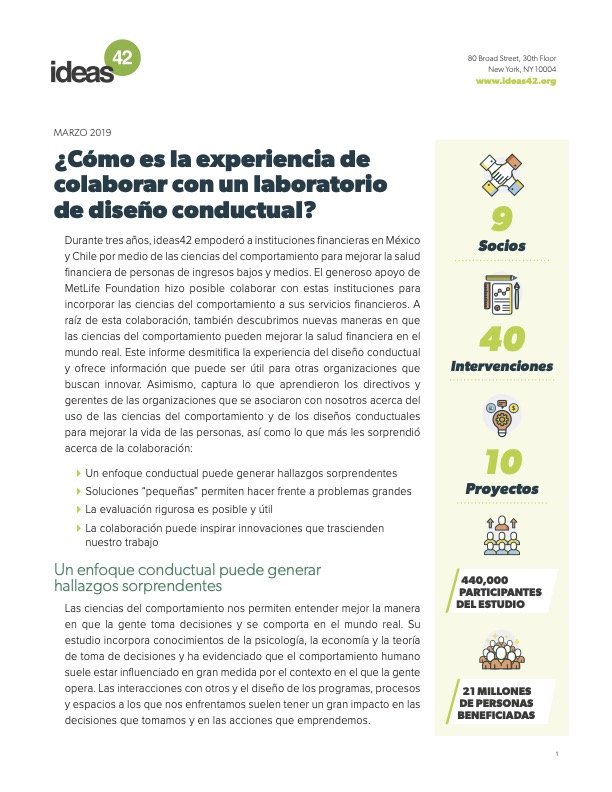

Policy Brief & Fact Sheet, Financial Health Cameron French 3/1/19 Policy Brief & Fact Sheet, Financial Health Cameron French 3/1/19 ¿Cómo es la experiencia decolaborar con un laboratoriode diseño conductual? Read More

Project Brief, Financial Health Leslie Heilbrunn 3/1/19 Project Brief, Financial Health Leslie Heilbrunn 3/1/19 What Is It Like to Partner with a Behavioral Design Lab? Read More

Report, Financial Health Leslie Heilbrunn 11/1/18 Report, Financial Health Leslie Heilbrunn 11/1/18 El uso de las ciencias del comportamiento para aumentar los ahorros para el retiro en México Read More

Report, Financial Health Kelsey Egger 11/1/18 Report, Financial Health Kelsey Egger 11/1/18 Using Behavioral Science to Increase Retirement Savings in Mexico Read More

Project Brief, Financial Health Leslie Heilbrunn 7/1/18 Project Brief, Financial Health Leslie Heilbrunn 7/1/18 The Financial Heuristics Training Read More

Report, Financial Health Leslie Heilbrunn 10/1/15 Report, Financial Health Leslie Heilbrunn 10/1/15 Using Behavioral Science to Increase Retirement Savings Read More